Suze Orman's All-Star Advice - Episode 2

Financial powerhouse Suze Orman helps decide what you can afford, when you should sign, how to handle money in a relationship and more.

This year, Suze wants you to live your best financial life. "I want this to be a time where every one of you gets that you can be the masters of your own financial destiny. The economy isn't going to be what saves you, and your government isn't going to save you. Nothing is going to save you but yourself. So let's make this a year with the information that you learn here, a year where you have the information to save yourselves." Let the advice-a-thon begin!Suze tackles the tough questions:

1. I want to buy a house, but in this economy, am I better off renting?

2. I remember when the emergency fund used to be six months. Now, you say eight months. Why do you keep changing it?

3. Where's the economy going? Is it getting better? Is it getting worse?

4. Now that we're married and trying to save for our family, should we continue to keep our finances separate? Or shall we merge them together?

5. How do you get financially intimate?

6. How many dates should you have before you start talking about money seriously?

7. What is FICO?

8. I have at least a hundred debt collectors calling me. I didn't know that having bad credit ruined my life. I need your help. What can I do to get out of this mess?

9. How well should I read something before I sign it?

10. What's your plan to help me live my best life in 2011?

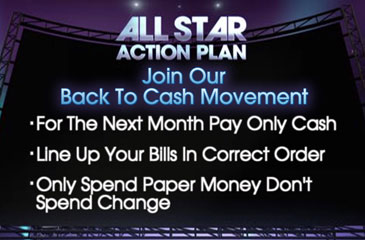

Plus, follow Suze's Action Plan: What you should do to start the New Year off right

Go to the first question